Considering an Offer to Retire Early: Should You Take It?

What is it?

In today’s corporate environment, where cost cutting, restructuring, and downsizing are the norm, many employers are offering their employees early retirement packages. As you near retirement age, you may find yourself confronted with an offer from your employer for early retirement. Your employer may refer to the offer as a golden handshake or a golden parachute. While many early retirement offers seem attractive at first, it is important for you to review an offer carefully before accepting it to ensure that it is indeed a “golden” opportunity.

Typical elements of an early retirement offer

In general

An early retirement offer usually consists of severance payments and post-retirement medical coverage coupled with already existing retirement benefits.

Severance payments

Severance payments are usually based on your salary and the number of years you have worked for the company. Severance payments can be distributed in either a lump sum or over a number of years.

Example(s): John has 30 years of service with the local utility company, and grosses $1,400 per week before taxes. When John reaches age 57, his employer offers him an early retirement package. The package includes a severance payment based on two weeks’ salary for each year that John worked for the company ($2,800 x 30 = $84,000).

Caution: In certain cases, severance pay is considered “deferred compensation” subject to the requirements of IRC Section 409A. Ask your employer if your severance package satisfies Section 409A. If it doesn’t, you could be subject to a 20% penalty tax.

Post-retirement medical coverage

Because of the high cost of medical care, you might find it hard to turn down an early retirement package that includes post-retirement medical coverage. These packages usually provide medical coverage until you reach age 65 and become eligible to receive Medicare. However, some packages continue to provide full or reduced medical coverage past the age of 65.

Bridging

Another type of early retirement offer is the Social Security “bridge payment.” Your employer provides you with temporary benefits to bridge the period between early retirement and the time when your Social Security benefits are scheduled to begin. The temporary benefits are usually equivalent to the amount you will receive from Social Security at age 62.

Example(s): John, age 57, works for a local utility company. The company offers John an early retirement package that includes five years of temporary benefits. These temporary benefits are equivalent to the amount that John will receive from Social Security at age 62. The benefits serve as a “bridge” between the period of John’s early retirement, age 57, and the period when he becomes eligible for early Social Security benefits at age 62.

Evaluating an early retirement offer

In general

The decision of whether to accept an early retirement offer is not an easy one to make. Your company’s personnel department may provide either individual or group counseling to guide you during this important decision-making process. If counseling is not available, you should speak to the person in charge of employee benefits at your company. Find out what amount you can expect to receive each year after you retire. Then, figure out the difference between what you would collect if you retire early and the amount you would earn if you continue working. Because they’re often the numbers used by employers to calculate how much money you’re going to receive, be sure that your company has your correct date of birth and starting date of employment.

Tip: If you choose to accept an offer for early retirement, some companies may pay (in the form of a bonus) all or part of the difference between what you would collect if you retire early and the amount you would earn if you were to continue working.

Caution: You should discuss your situation with an attorney and/or financial professional. Although a company-paid consultant may provide valuable information, they may not necessarily be acting in your best interest.

Tax/retirement plan implications

If you accept an early retirement offer, you should be aware of any possible tax implications. Defined benefit plans often contain provisions that reduce your monthly benefit when you begin distributions before a certain age. As a result, early retirement can result in lower monthly retirement benefits. Taxable distributions from employer-sponsored retirement plans [such as 401(k)s] and IRAs are generally subject to a 10% premature distribution tax if made before age 59½. However, there are a number of exceptions to this rule. One important exception is for distributions made from 401(k)s and other qualified plans as a result of separation from service in the year you reach age 55 or later (age 50 for qualified public safety employees participating in certain state or federal governmental plans). Another important exception to the 10% premature distribution tax is for substantially equal periodic payments (sometimes called SEPPs). Substantially equal periodic payments are amounts you receive from your IRA or qualified retirement plan not less frequently than annually for your life (or life expectancy) or the joint lives (or joint life expectancy) of you and your beneficiary. There is no minimum age requirement for this exception, but distributions from qualified retirement plans are eligible for the exception only after you separate from service.

Provided that you’re over age 59½ or meet one of the exceptions, you can make penalty-free withdrawals from your account/plan. However, you may still have to pay income tax on all or part of the withdrawal. Distributions from employer-sponsored plans are usually taxable, since contributions to most of these plans are made on a pre-tax basis (although qualified distributions from Roth 401(k)s and Roth 403(b)s are free from federal income taxes). IRA distributions may or may not be taxable, depending on whether or not the contributions you made to the account were tax deductible. Roth IRAs are subject to special rules of their own.

Tip: While withdrawals from an IRA or retirement plan can be a valuable source of retirement income, the need for current income should be weighed against issues such as: (1) the desire to defer income tax for as long as possible, (2) the desire to preserve the assets for your beneficiaries, and (3) the possibility that, with life expectancies on the rise, you may live into your 80s or 90s and may, therefore, need to draw on those retirement assets for a long period of time.

Consequences of saying no to an offer

If you’re thinking about turning down your employer’s offer to retire early, be aware of the consequences. If you’re holding out for a better offer, keep in mind that the first offer is oftentimes the most generous. Also, if you think there is a good chance you might be let go anyway down the road, you may want to accept a sure thing right away rather than face the uncertainty of your company’s future plans.

Consequences of saying yes to an offer

In general

After careful consideration, you may find that early retirement is the way to go. However, before you jump right into retirement, you’ll want to be aware of the consequences of saying yes.

Less time to save for retirement

If you accept an offer to retire early, say at around age 55, you could be giving up 10 years or more of saving for retirement. Less time to save means you will have fewer savings available during retirement.

Example(s): John saves $700 a month in a tax-deferred retirement plan at a 7% annual return for 20 years. At age 55, his retirement savings will have grown to approximately $366,780. If John leaves that money in his account for another 10 years and earns the same 7% annual return, even without any additional contributions his savings will grow to approximately $737,100. If John keeps contributing for the additional 10 years, his retirement savings could be even more. (This is a hypothetical example, and is not intended to reflect the actual performance of any specific investment, nor is it an estimate or guarantee of future value. Investment fees and expenses have not been deducted; if they had been, the accumulation totals would have been lower.)

Retirement savings will have to last for a longer period of time

A lower retirement age, coupled with generally increasing life expectancies, can result in your retirement years making up one-third of your total life span. In other words, you could spend as many years in retirement as you did in the workforce. Your retirement savings will have to last for a longer period of time than if you had retired at the normal retirement age. In addition, you should consider the effect of inflation, which could eat away at the purchasing power of your retirement savings.

Your pension may be smaller

If you participate in a traditional defined benefit plan, also known as a pension plan, accepting early retirement could result in a smaller pension. You should determine whether it is more valuable to have a smaller benefit over a longer period of time rather than a larger benefit over a shorter period of time. Generally, defined benefit plans are based on two factors: (1) length of service, and (2) salary during your highest earning period. If you retire early, your years of service are reduced. In addition, most employees’ highest earning period occurs just before retirement, so early retirement can force you to give up your highest earning period. Furthermore, many companies impose early withdrawal penalties that can equal 5% to 7% of your pension for each year that you retire early.

On the other hand, employers sometimes sweeten early retirement packages, increasing your pension benefit beyond what you’ve earned by adding years to your age, length of service, or both, or by subsidizing your early retirement benefit or your qualified joint and survivor annuity option. These types of pension sweeteners are key features to look for in your employer’s offer — especially if a reduced pension won’t give you enough income.

Psychological impact

In addition to determining whether or not you have the financial resources to retire, you should also consider the psychological impact of retiring early. One of the first questions that you need to ask yourself is: Am I really ready to retire? Early retirement thrusts you into a lifestyle change that you may not have expected to encounter for another 10 to 15 years. You may find it difficult to adjust from a working environment to a relaxed, laid-back lifestyle. While many people will find it easy to adjust to a lifestyle that includes vacations and golfing, others may have a hard time dealing with all the free time.

Fortunately, there are ways for people who have a difficult time coping with this sudden change in lifestyle to ease themselves into retirement. Not only can a part-time job provide you with extra cash, but it can also help keep you busy.

Career counseling

What if you can’t afford to retire? Finding a new job

You may find yourself having to accept an early retirement offer, even though you can’t afford to retire. One way to make up for the difference between what you receive from your early retirement package and your old paycheck is to find a new job, but that doesn’t mean that you have to abandon your former line of work for a new career. You can start by finding out if your former employer would hire you as a consultant. Or, you may find that you would like to turn what was once just a hobby into a second career. Then there is always the possibility of finding full-time or part-time employment with a new employer.

If you have been out of the job market for a long time, you might not feel comfortable or have experience marketing yourself for a new job. Some companies provide career counseling to assist employees in re-entering the workforce. If your company does not provide you with this service, you may want to look into outplacement firms and nonprofit organizations in your area that deal with career transition.

Caution: Many early retirement offers contain non competition agreements or offer monetary inducements on the condition that you agree not to work for a competitor. However, you should be able to work for a new employer and still receive your pension and other retirement plan benefits.

Retirement planning issues

Medicare — age 65

Even though you can receive early Social Security retirement benefits, you are not eligible for Medicare benefits until age 65. If your early retirement package does not include post-retirement medical coverage, you may have to look into alternative methods of obtaining health benefits, such as through COBRA (Consolidated Omnibus Reconciliation Act of 1985) or private health insurance, until you are eligible to begin receiving Medicare benefits.

Social Security — age 62

If you accept an early retirement offer, you might want to consider applying for early Social Security retirement benefits. The Social Security Administration allows any individual who is eligible to receive Social Security benefits at full retirement age the option of receiving benefits beginning at age 62. However, if you decide to receive Social Security benefits before full retirement age, the benefits you receive will be reduced.

Tip: If you accept an early retirement offer from your employer, you are not required to begin receiving early Social Security retirement benefits before full retirement age.

Can you afford to retire early?

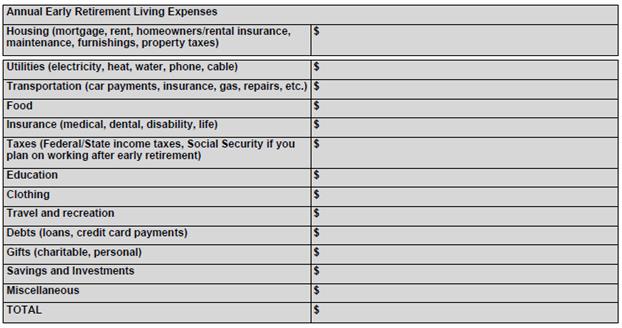

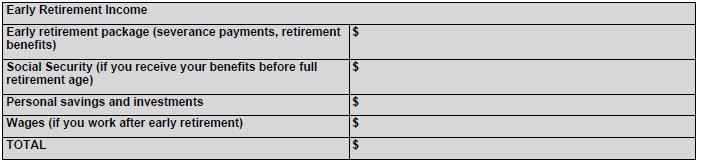

Whether or not you have the financial resources to retire early depends on how much you have in retirement income and how much you plan to spend when you retire. Your early retirement income includes your early retirement package (severance payments and retirement benefits), Social Security (if you receive benefits before full retirement age), personal savings and investments, and wages (if you work after early retirement). To determine how much you will spend, you must estimate your annual living expenses for early retirement.

It is important to note that your annual living expenses during early retirement are likely to differ from your expenses later in retirement. During early retirement, you may find yourself still paying off a mortgage, funding your children’s education, and paying for medical coverage. The worksheets that follow can help you to estimate your early retirement income and living expenses, and determine whether or not you can afford to retire early.

Caution: If your early retirement package does not include medical coverage, remember to calculate the cost of health care into your early retirement living expenses.

Tip: When you estimate your early retirement living expenses and income, it is important to consider inflation, which has historically averaged approximately 2% annually over the past 20 years, according to the Bureau of Labor Statistics (as of January 2019).

Financial concerns

Loss of health insurance

If your early retirement package does not include company-paid health benefits, you still may be eligible for health insurance through COBRA. You are entitled to COBRA coverage if you work for a company that provides employees with a group health plan and has 20 or more covered employees. COBRA allows you to pay for your health insurance at the same rate your company pays, plus a small administrative fee. COBRA coverage generally lasts up to 18 months from the date of retirement, and does not require you to qualify for coverage or worry about pre-existing conditions. Once your COBRA coverage runs out, you will have to purchase private insurance if you want to continue health insurance coverage until you are old enough to qualify for Medicare coverage.

You also may shop for and purchase an individual health insurance policy through either a state-based or federal health insurance Exchange Marketplace.

Reduction in Social Security benefits

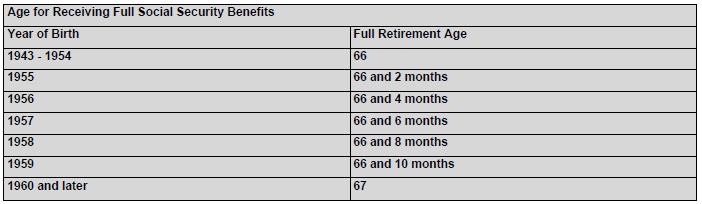

Your Social Security benefits are based on what is known as the primary insurance amount (PIA). The PIA is based on your average indexed monthly earnings (AIME). If you retire at the full retirement age (see the following Social Security Administration table), your monthly benefit will be equal to your PIA. However, if you receive your Social Security retirement benefits early, your monthly benefit will be less than your PIA.

If you elect to receive Social Security retirement benefits early, you can receive more benefit checks than if you retire at full retirement age. While this might seem profitable, you will suffer a permanent reduction in your monthly benefits. The reduced benefit is based on a deduction of approximately 5/9 of 1 percent (.0056) for each month you receive benefits before full retirement age up to 36 months, and a deduction of 5/12 of 1 percent thereafter. Your total lifetime benefits would remain the same based on standard life expectancy assumptions. However, your benefits are spread out over a longer period of time, which results in lower monthly benefits.

Example(s): Mary retires from the local utility company at age 63, and elects to receive her Social Security benefits early. If Mary had waited to receive her Social Security benefits until her full retirement age of 66, she would have received 100% of her primary insurance amount (PIA) benefit, or $800. Because Mary elected to receive her benefits at age 63, there is a reduction of 5/9 of 1 percent (.0056) for each of the 36 months that she receives benefits prior to full retirement age. Thus, Mary will receive approximately $640, or 20% less (.0056 x 36), than she would have received at normal retirement age.

Tip: The application process for early Social Security retirement benefits can take as long as three months. The Social Security Administration recommends that you contact its office prior to your 62nd birthday.